Earlier today, the district closed on the sale of 22 million in bonds. The District sold the bonds to refinance its outstanding 2014 General Obligation Bonds on October 7th, and it went exceptionally well. The district pursued this option due to the current 10 year treasury rates that made it advantageous for our taxpayers.

Overall, the District locked in savings of $1.3 million on a present value basis and over $1.57 million over the remaining duration of the 2014 bonds, by locking in a new borrowing rate of 2.27%. This rate was in contrast to the average coupon borrowing rate of 5% on the bonds being refinanced. The bonds were extremely popular with bond buyers – in fact, at the end of the order period there was $123 million in orders, even though the District was only selling $22 million! As a result, the underwriter, Piper Sandler, was able to reduce the interest rates from the original offering levels.

The high demand among investors was in large part due to the strong credit rating of the District, a level of “A1” from Moody’s Investor’s Service. In their rating write-up, Moody’s specifically cited the District’s solid financial position.

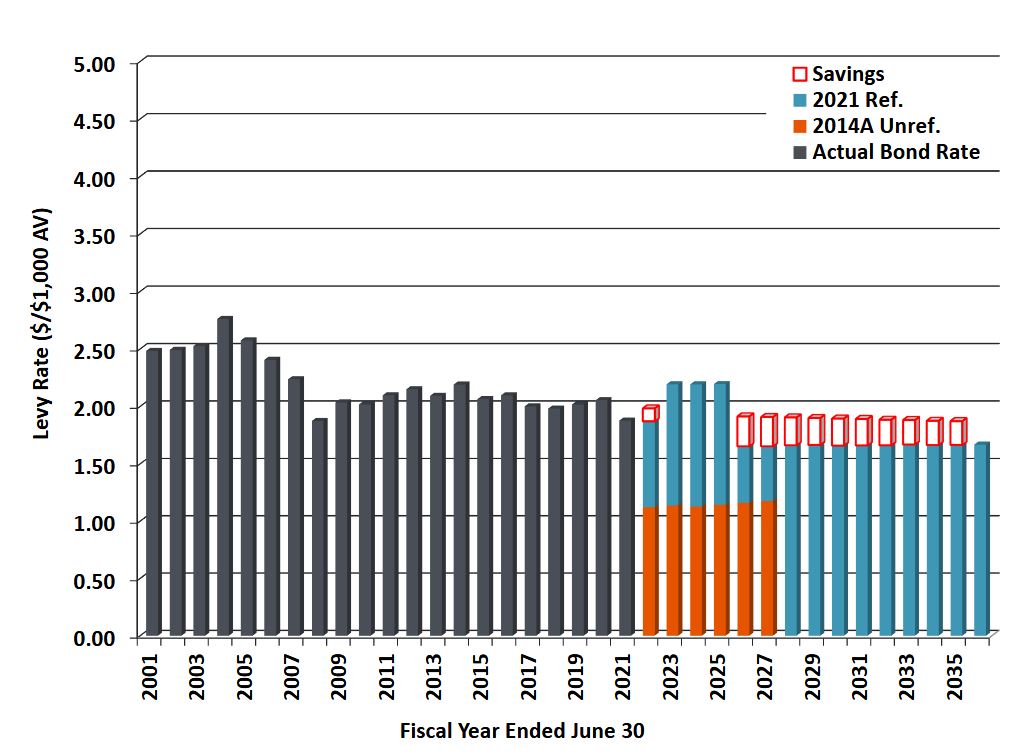

For the next three years, our bond rate is expected to be at the $2.19/$100,000 level (what was promoted when our last bond was passed in 2014) Following that, the rate for area taxpayers is predicted to drop below the $1.65 level through the duration of the debt. Below is a chart depicting this transaction, and the savings to local taxpayers.

Leave a Reply